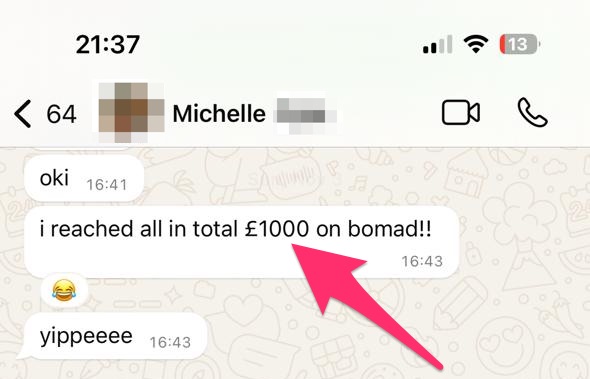

My daughter Michelle (10) noticed that she’d achieved this milestone just a few days ago:

£1,000 isn’t actually the total of her Bomad accounts (the money we owe her), but the sum of that and her “external accounts”.

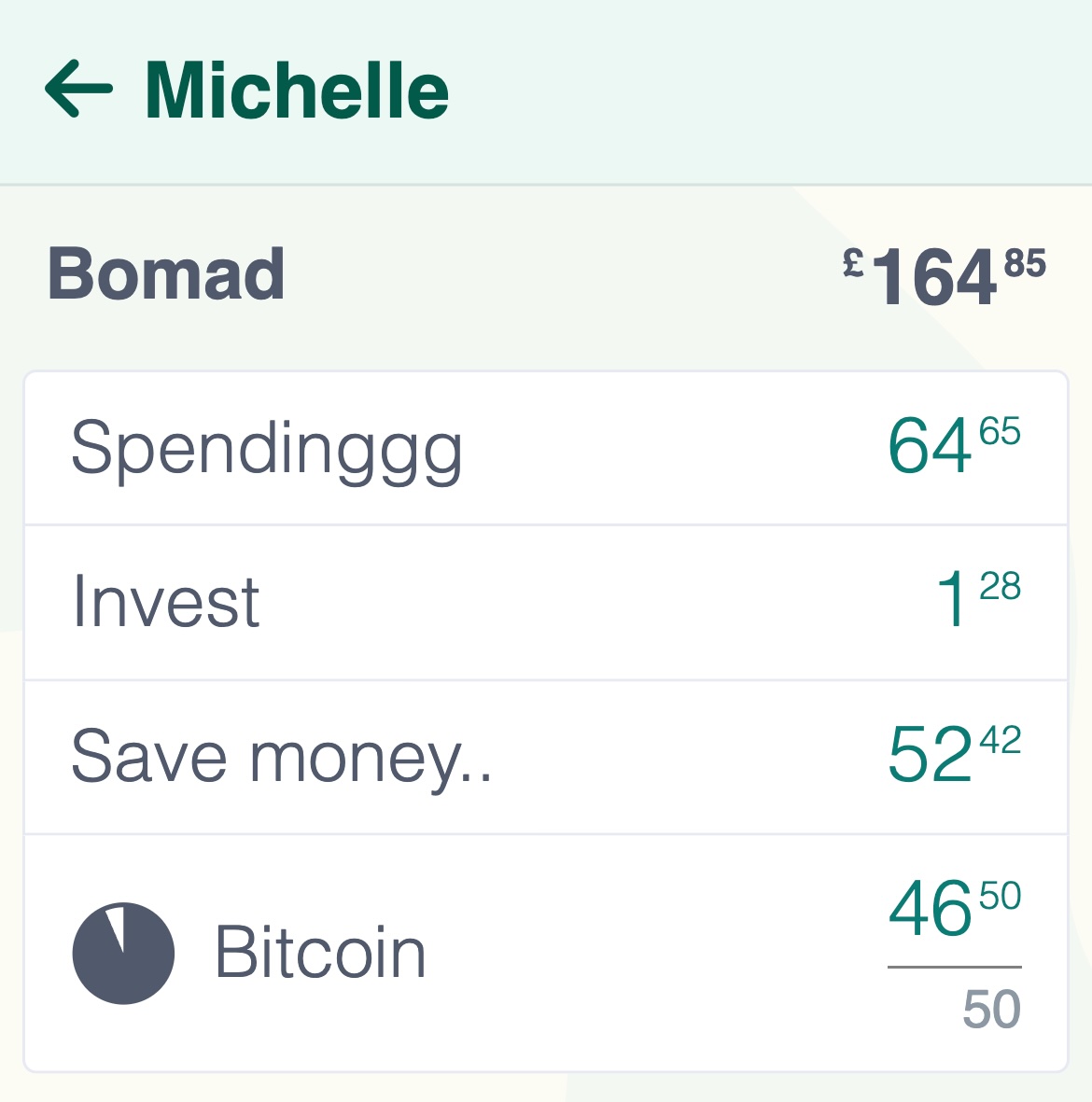

Let me explain. Currently, her Bomad accounts add up to £164. She has organized them into a few sub-accounts:

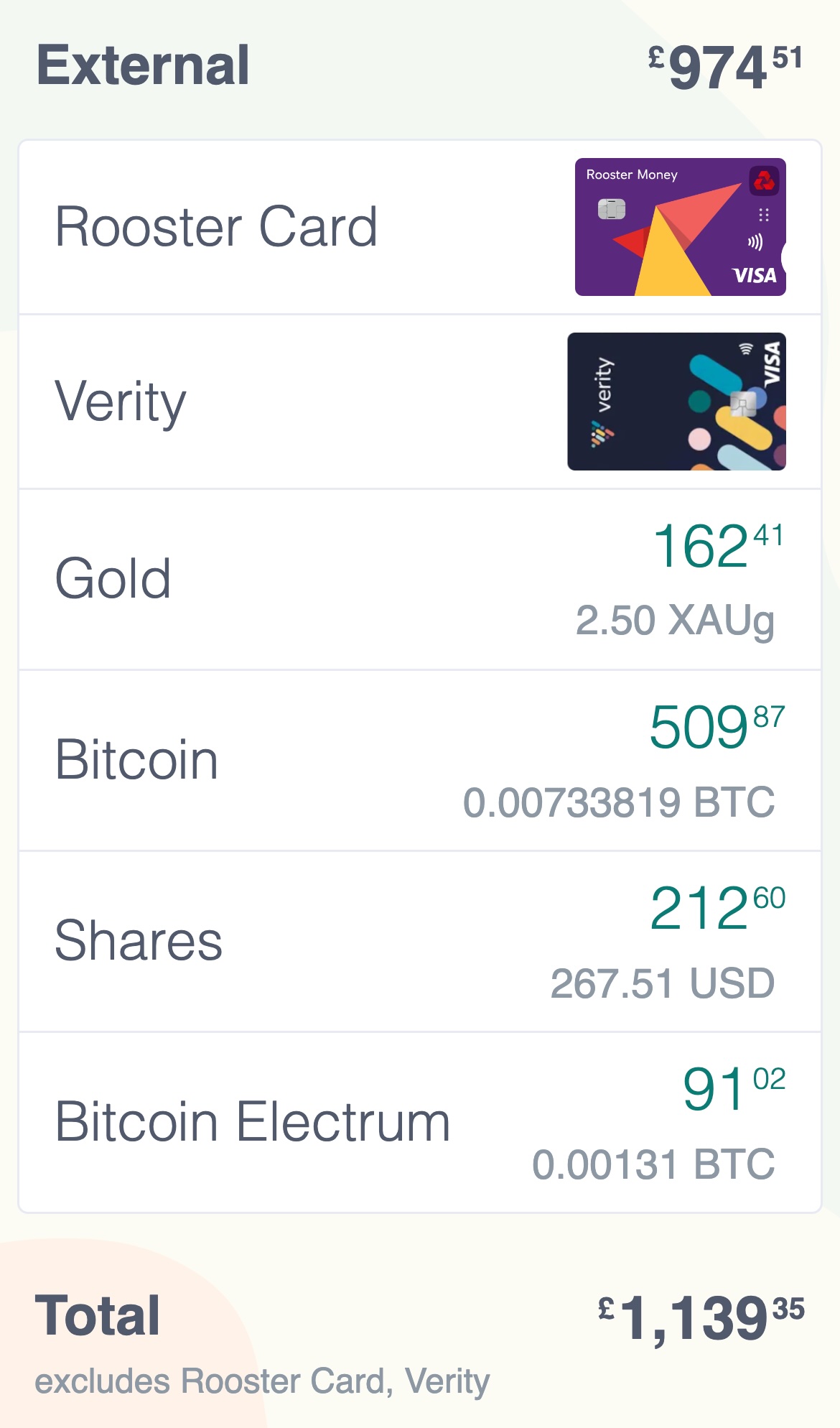

In addition to that, her “external accounts” are also listed in Bomad. This isn’t money that we owe her, but rather the value of assets like gold, stocks and Bitcoin that belong to her:

Money in an actual bank or savings account is also considered to be an external account. She has two such accounts with debit cards, but the balance is generally low and we don't track it in Bomad.

As you can see, her net worth (Bomad £164 + external accounts £974) has jumped to £1,139, mainly due to the recent Bitcoin price increase.

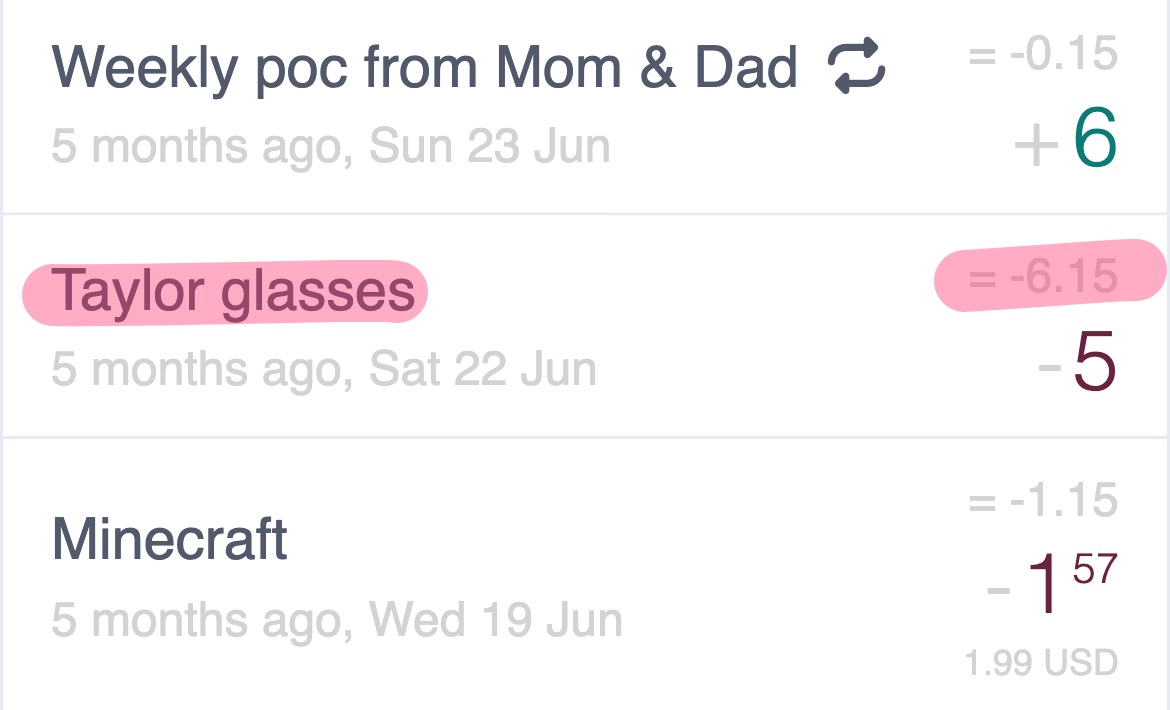

I didn’t actually think she was paying much attention to her net worth. She’s always had a keen eye on her spending account (called “Spendinggg” above) because that’s the limit of what she can spend. We even allowed it to go negative in the past under very special circumstances, like when she bought sunglasses at the Taylor Swift concert:

Now she's back to a very healthy £64 in that same account. Perhaps that, together with her starting to track her net worth, is evidence that she’s maturing 🤗

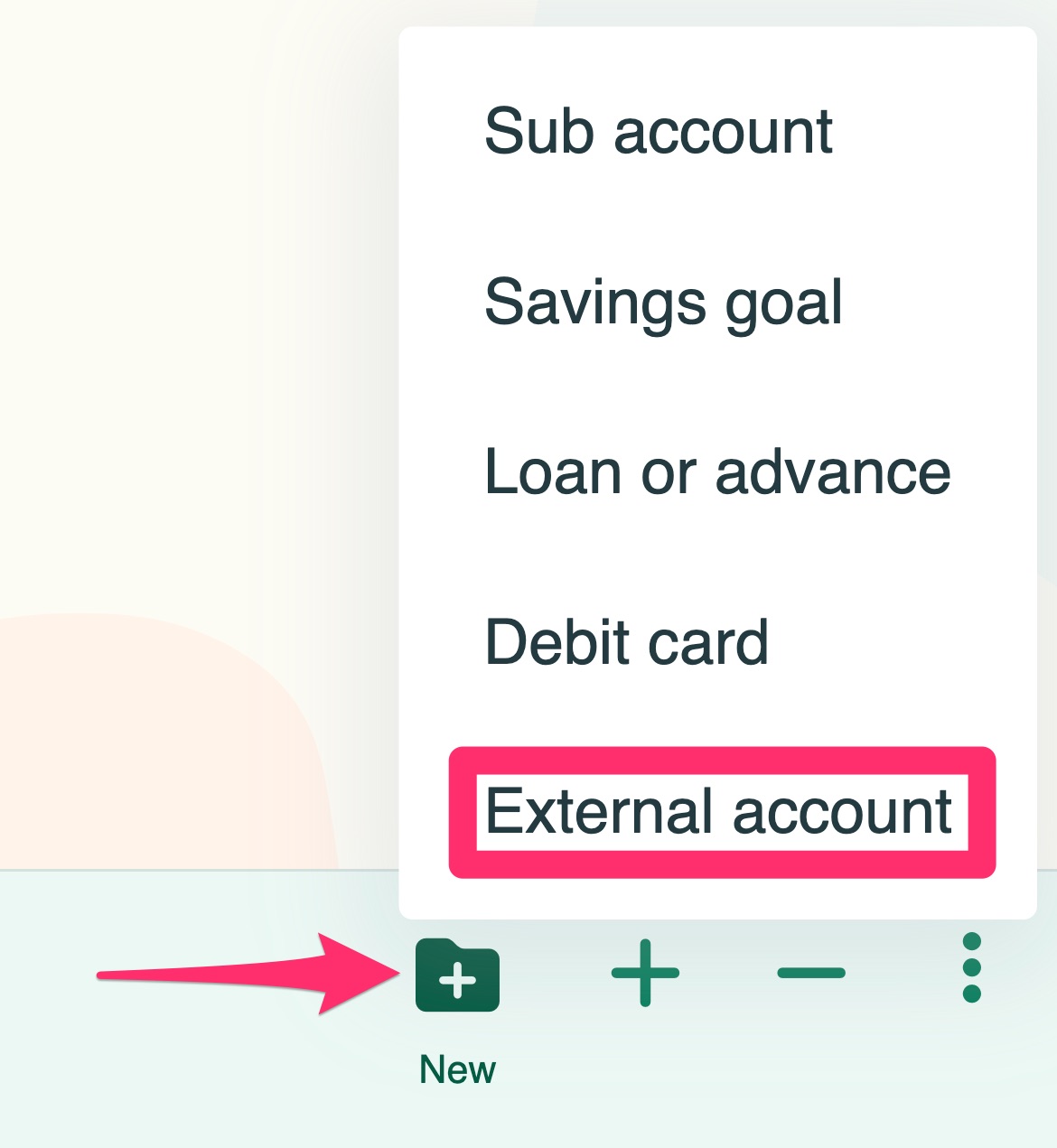

In case you haven’t tried it, you can add “external accounts” to Bomad as below:

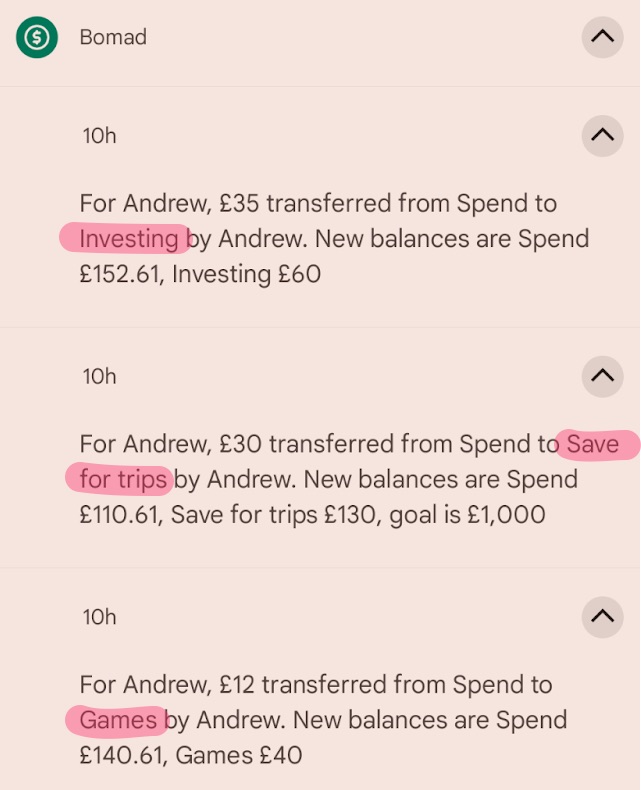

I’ve been similarly impressed with my son Andrew (16). A few weeks ago, I got the following notifications from Bomad on my phone (I’ve marked the sub-accounts for later reference):

So he’s been quietly organizing his money by himself. Good lad!

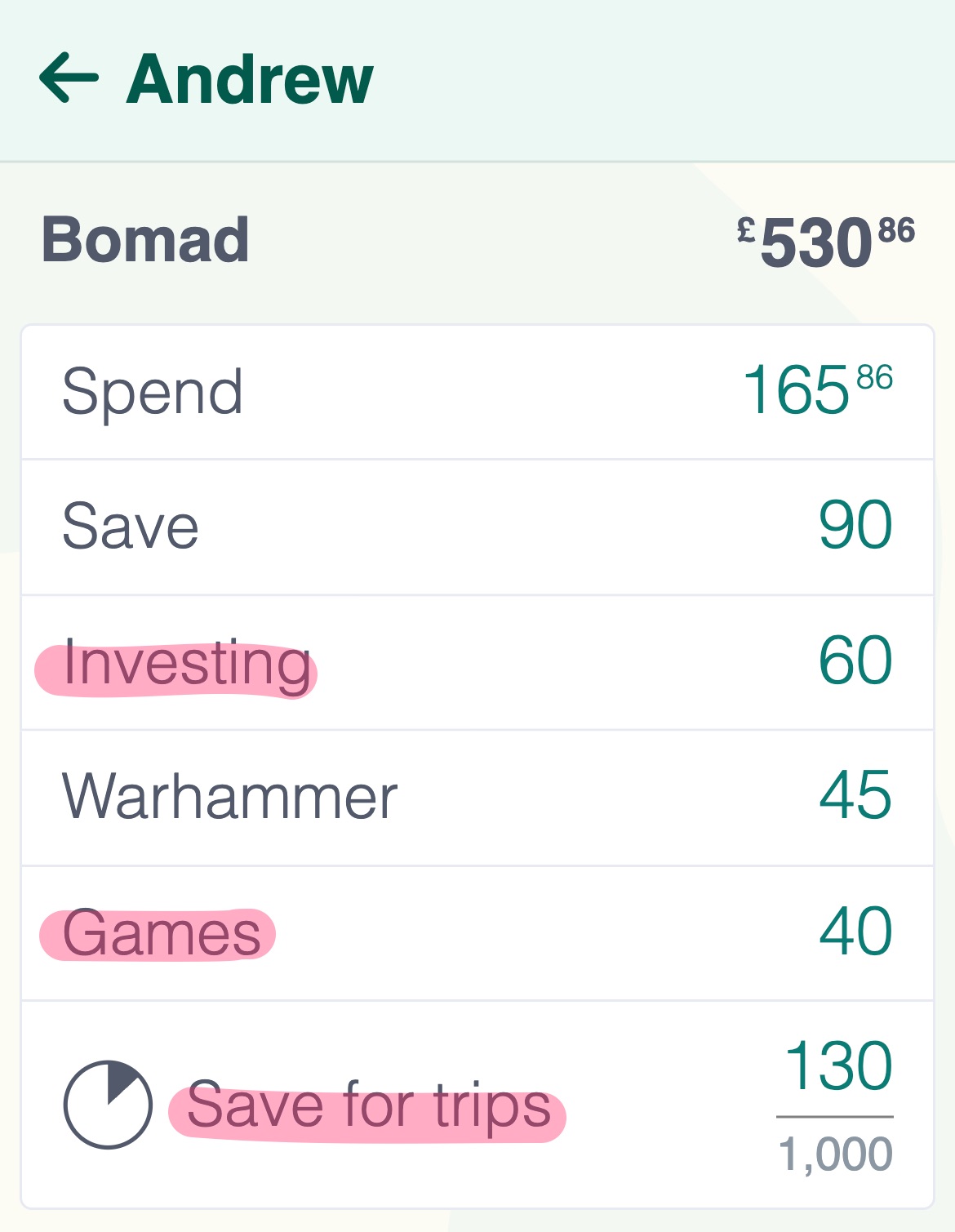

Here’s what his Bomad accounts look like. You can see the Investing, Save for trips and Games sub-accounts that were mentioned in the notifications above:

He’s started paying for most of his day-to-day spending from his own bank account. He earns a fair amount from babysitting one of the younger kids at his school. This gets paid directly into his bank account. He also gets paid cash for helping out in the school kitchen. None of this is reflected in Bomad.

I suspect he enjoys the privacy. Or perhaps he trusts the bank more than an IOU from his parents 😉

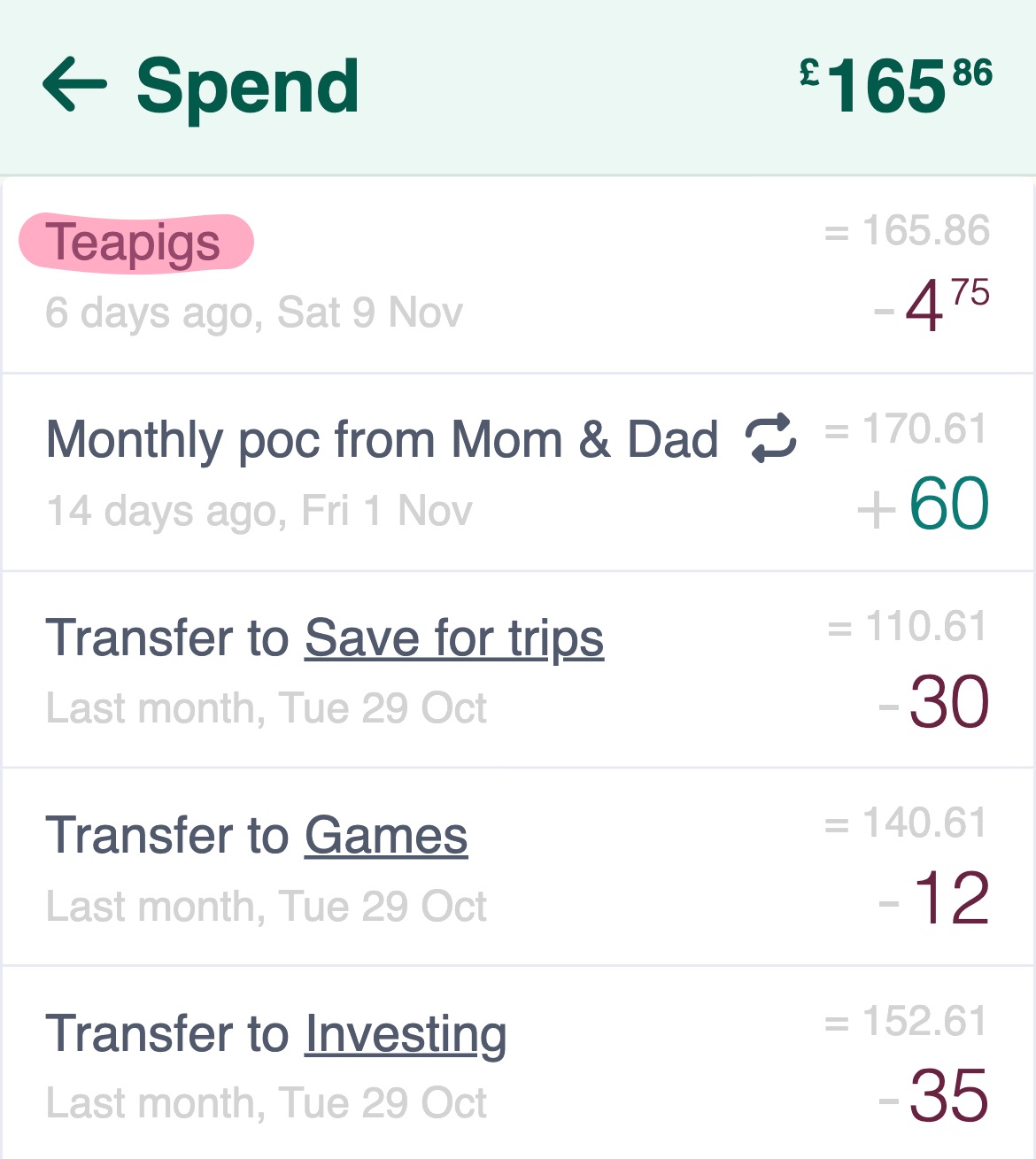

His allowance, however, still gets paid into Bomad, and Bomad is still quite useful for when he throws certain items into the shopping cart, like he did this weekend for some fancy tea bags he wanted ("teapigs"):

All in all, I’m quite satisfied with how both my kids are engaging with money. I am rather confident that they’re on track to have a positive relationship with money as adults. I think they’re going to be much better off than most kids who are shielded from making any financial decisions, and then dropped in the deep end as young adults.

One area for improvement is investments. Having gotten the basics nailed, this is something I’ve only turned my attention to recently. And I’m not talking about teaching them to make clever stock picks, etc, but rather about developing the HABIT of taking some of your income and investing it in order to grow your financial resources over time.

More about that next time!